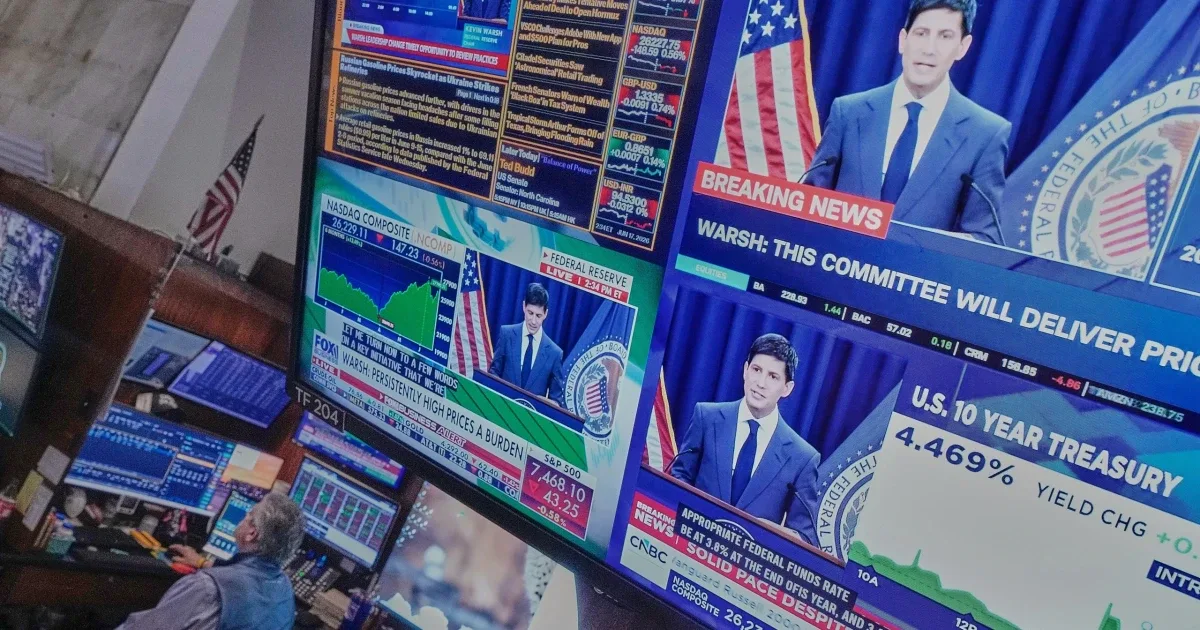

Global equities experienced a widespread selloff as investors recalibrated expectations for U.S. interest rates, responding to Federal Reserve projections that suggested a prolonged period of higher rates. Technology stocks and growth-oriented sectors bore the brunt of the market decline, reflecting concerns about sustained borrowing costs.

Europe’s STOXX 600 index fell notably, led by losses in semiconductor and chip-equipment companies. U.S. futures linked to Nasdaq suggested an extension of recent declines in major technology benchmarks. The Federal Reserve’s latest statement kept the benchmark interest rate steady but revealed that half of its policymakers foresee at least one rate hike in 2026. Additionally, the interest rate paid on bank reserve balances was set to remain elevated, reinforcing the expectation of continued tight monetary conditions.

The market shift signals slower relief on consumer borrowing expenses such as mortgage rates and credit cards, exerting pressure on households with fluctuating debt costs. Investors with portfolios heavily weighted in high-valuation technology stocks also adjusted their outlook, further driving market volatility.

Asian markets mirrored this sentiment, with South Korea’s KOSPI posting its most significant single-day drop since March, primarily driven by semiconductor stock selloffs. The Japanese yen hovered near a four-decade low against the dollar after officials flagged readiness to intervene in currency markets. This market-wide repricing extended beyond stocks, affecting bonds, currencies, and commodities.

Oil prices continued their monthly decline, nearing levels not seen since early spring. Brent crude fell below $77 per barrel amid a sharp correction that, if sustained, could eventually ease fuel costs for consumers. Despite this, the prevailing mood remains cautious as the market wrestles with the implications of "higher for longer" interest rates.

Investors today are treating the Federal Reserve’s message as a reality check, with stronger earnings and AI-driven growth still rewarded, but with much less tolerance for overvalued assets in a tight monetary environment. The prospect of cheaper borrowing this year appears increasingly uncertain, even as lower energy prices offer some respite to consumers facing inflationary pressures.